{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.title}}

{{item.text}}

We can support customers with a comprehensive and multidisciplinary approach involving professionals from strategic, operational and technological business areas.

Our differentiating E2E competencies help customers in identifying tailor-made use cases through innovative methodologies, defining competitive strategies and operating models, designing technological platforms and supporting the necessary cultural shift.

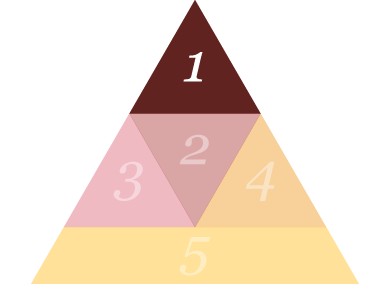

What?

Understanding final customer behaviour in advance thanks to the information at Banks’ disposal, but also integrating information form other sources

How?

Identification of use cases and related user experience studying the best practices of the market and analysing the available information assets

Why?

7 consumers out of ten would like to receive real-time offers tailored on their needs(1)

74% of financial institutions see data analytics as the most relevant technology to invest on(2)

(1) PwC Total Retail, 2017 | (2) PwC Global FinTech Report, 2017

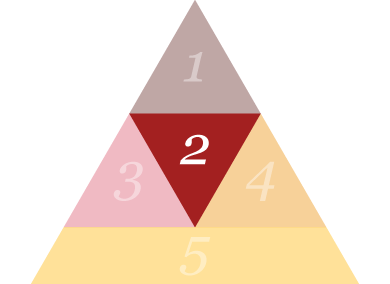

What?

Development of new open business and service model, leveraging the collaboration with other players, even outside the banking ecosystem

How?

Definition of the Open Banking strategy identifying the market potential and the possible collaboration models to be adopted (ecosystem TOM)

Why?

45% of financial institutions are currently engaged in partnerships with FinTechs(1)

82% of financial institutions expect an increase in partnerships in next 3-5 years(1)

(1) PwC Global FinTech Report, 2017

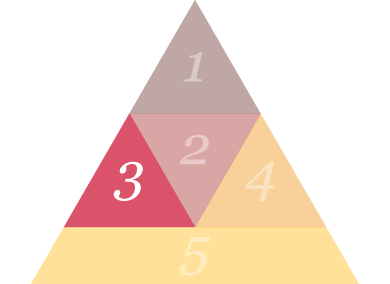

What?

Evaluating which revenue and business models to adopt, moving the perspective toward the final customer and leveraging from the web experiences (e.g. API monetisation)

How?

Definition of the business models, of the new commercial offer features and of the entry strategy into the market

Why?

New revenue streams are becoming more relevant for Banks: in particular, despite lower interest margins, the commission component on total revenue increased from 26% (2008) to 38% (2017)(1)

(1) PwC analysis on public financial statements, 2017

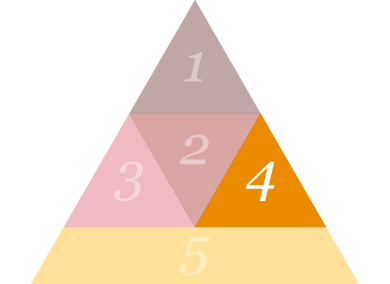

What?

Customer engagement and constant feedback measurement to ensure clients an experience of services, solutions, responses along the entire journey

How?

Definition of an effective customer experience management process which leverages constant monitoring of customers’ expectations and feedbacks

Why?

New digital players capture clients’ feedbacks analysing it in real-time to address new opportunities. Therefore, Banks should cultivate the ability to react in time to close the gap between expectation and experience

What?

The foundation to realise an Open Banking model is a renewed firm culture, implying deep changes in traditional financial institutions’ DNA to move out of the traditional patterns

How?

Portrayal of the identified Open Banking TOM, designing “thin” decisional processes and hiring people with innovative mindset (even from other industries)

Why?

55% of FinTechs noticed gaps in management and culture when working with Banks(1)

77% of financial institutions are willing to increase their innovation effort in next 3-5 years(1)

(1) PwC Global FinTech Report, 2017

Combining these ingredients, Banks can build up a proper Open Banking strategy

Financial Services players should approach Open Banking starting from data exploitation to discover new needs and create new offering systems

An effective Open Banking strategy should be based on a renewed and improved corporate culture

The Financial Services industry is living a time of profound transformation and its players face every day the changes overwhelming the market. New customers’ needs and habits, new players in the Financial Services market, new technologies (e.g. APIs, Analytics) and rules (e.g. PSD2, GDPR) are pushing incumbents to revise their models to maintain their positioning and keep up margins.

Banks are opening their IT infrastructures and sharing the customers’ information, based on the regulation and the customer consents, in order to be able to compete with always more customized services and renewed experiences for their clients.

This situation leads the banking industry to the next level of evolution: the Open Banking era. Hereafter, we aim to provide a global overview of the market, showing where different Countries stand in the Open Banking landscape.

The spark that triggered the Open Banking revolution is different from Country to Country. While in some Countries Open Banking developed out of the necessity to be compliant with new regulations, in others it began due to incumbents understanding and taking advantage of the benefits of innovation.

The factors originating Open Banking can therefore be divided in four categories:

Approaching innovation proactively through the redaction of ad-hoc laws and regulations can help in generating a level playing field and the necessary underlying circumstances for the flourishment of Open Banking.

This is the case of the European Countries, where incumbents started approaching Open Banking model following standards introduced by PSD2. The regulation of TPP and the introduction of dedicated Guidelines and Regulatory Technical Standards of communication paved the road to a renewed approach of collaboration.

However, by extending the scope of our analysis to Countries overseas, we can see a different example in Mexico, where the Government decided to start its regulatory process with dedicated laws on newcomers such as “FinTechs” rather than proceed with the regulation of the overall market.

This shows how the regulatory push can be driven both by the need for a comprehensive regulated framework, and by the specific needs of the Country; in both cases the result is however a push towards Open Banking approach.

Players of the banking sector historically haven’t been much proactive towards change: banking services have always been seen as settled, with little room for improvements. Even if some innovations were introduced over the years, such as banking Apps or contactless payments, the main services and business models have remained unchanged. One of the reasons why this happened is the absence of players introducing an innovative approach and trying to modify the playing field changing market perspectives.

Open Banking is set to change that.

An example comes from the United Kingdom, where after the nine biggest Banks were forced to adopt an Open Banking model and expose their APIs, other Banks and market players started implementing a similar model to remain competitive in the market and be able to offer an always more customized user experience.

Another push could be seen in the advent of Digital Banks coming to the market with an innovative and digital offer, profoundly different to that of traditional Banks. Customers now approaching the financial sector for the first time (e.g. Generation Z) are much more likely to be attracted by the offer of a Digital Bank.

Incumbents, if they don’t want to lose out, need to comprehend and adapt to this ever-changing competitive scenario.

The development of APIs to connect Banks with third parties, thus creating an ecosystem of services, the need for security in the transactions field and in data sharing initiatives, as well as the necessity of a sound data management and data analytics tools, all contributed to the definition of a new technological landscape.

Traditional Banks, which started operating in a completely different market, face the difficulty of changing their legacy systems to compete with the lean and agile organization of newcomers.

Therefore, some Countries decided to approach Open Banking starting just from the creation of standardized APIs, seeing this process as a way to facilitate the transition to an Open Banking ecosystem. Examples of this are Switzerland and Nigeria, which considered this approach to be more effective.

Incumbents face the necessity to leverage emerging technology enabling solutions for the creation of value-added services.

In the ever-changing and customer-centric world we live today, customers are expecting always higher standards of service, with tailor-made offers and instant solutions to their problems.

The banking industry is no exception. The advent of new players has made evident that adaptation and agility towards change are key features to maintain a primary role in the Financial Services market.

If incumbents want to retain customers and attract new ones, they need to understand what their clients’ needs are, being them explicit or not.

An example of companies figuring this out comes from China, where the biggest player of the market successfully created an ecosystem revolving around customers. One of them introduced in his messaging app different functionalities for various moments of its users’ life, like paying bills, e-commerce, in-store payments, and others.

These companies, which did not belong to the financial sector, had the capabilities to create innovative services that are now substituting operations previously carried out by Banks.

Customers’ expectation in the fruition of services has changed: they got used to receiving the best service possible as soon as they need it in any sector and they now expect the same experience from the banking sector as well.

In all the Countries considered, the need for a regulatory framework and API standards has been recognized, and most Governments are moving in that direction. However, it is important to highlight that the state of advancement and the approach utilized varies greatly from Country to Country: while some have already implemented new ad-hoc laws and API standards, others are still working towards that goal

Customers are used to high level service standards and to tailor-made offers and are now expecting the same from the Financial industry. Banks are approaching new technologies (such as Data Analytics) enabling the creation of customized offers also answering to latent customer needs. It is now clear that operating through the creation and sale of generic products to customers is no longer a possibility to compete in the market

While there is a general acknowledgement of the necessity of change, only some Banks embraced it completely, experiencing an overall change in their firm culture. Leaders in the Open Banking scenario are those Banks characterized by an evolution of their mindset. This change is pushing them towards a multidisciplinary approach, to the development or acquisition of new competences and to the creation of dedicated innovation departments